Discover everything about commercial food truck insurance – cost, coverage, providers, and how to get insured. A 2025 guide for food truck businesses.

Running a food truck is an exciting way to bring great food directly to customers, but it also comes with real risks. From kitchen fires and customer injuries to auto accidents and equipment theft, a single unexpected event can shut your business down overnight.

That’s why food truck insurance is important—not just to meet legal requirements, but to protect your investment and livelihood.

If you’re asking, “Do you need insurance for a food truck?”—the answer is yes. Most states require certain types of insurance to operate legally, and event organizers often demand proof of coverage before letting you set up.

Beyond legal compliance, having the right insurance helps cover costly damages and liabilities that can arise on the road or during service.

In this guide, we’ll break down everything you need to know about commercial food truck insurance—including the different types of coverage available, how much it costs, what to look for in a provider, and where to get started in 2025.

What is Commercial Food Truck Insurance?

Commercial food truck insurance is a specialized type of business insurance that protects mobile food vendors from financial losses caused by accidents, injuries, theft, property damage, and other risks that come with operating a food truck. Unlike basic commercial auto insurance, this policy is tailored for the unique needs of mobile food businesses.

If you’re running a taco truck, coffee trailer, BBQ van, or ice cream truck, you need more than just auto coverage—you need protection for your kitchen equipment, employees, and the food you serve. This is where insurance for mobile food vendors becomes essential.

Most people search online for “what is commercial food truck insurance” when they’re first launching their food truck business or getting ready to participate in large public events or festivals. Understanding this type of insurance helps you make smart decisions that keep your business safe and compliant.

Whether you operate a food trailer, food cart, or fully equipped truck, commercial food truck insurance typically includes:

- General Liability Insurance – Covers third-party injuries and property damage.

- Commercial Auto Insurance – Covers vehicle-related accidents and damages.

- Property Insurance – Covers your kitchen equipment, appliances, and inventory.

- Workers’ Compensation – Required if you have employees, covering job-related injuries.

This coverage is especially important if you’re wondering about the difference between food truck vs food trailer insurance—because while both operate under similar risks, their insurance needs can vary depending on whether the vehicle is self-propelled or towed, and whether it’s used for cooking, storage, or both.

Why You Need Food Truck Insurance

If you’re serious about running a food truck business, getting the right insurance isn’t optional—it’s essential. From state and city regulations to unexpected lawsuits or property damage, food truck insurance is your financial shield. Without it, a single incident could wipe out everything you’ve worked for.

Legal Requirements in Most States

In many U.S. states, certain types of food truck insurance coverage are legally required, especially commercial auto insurance and general liability insurance. For example:

- If your food truck is driven on public roads, you must carry commercial vehicle insurance (just like any other business vehicle).

- Many health departments and local municipalities require proof of liability insurance before issuing a food vendor permit.

- If you employ staff, you may also be required to carry workers’ compensation insurance.

According to the Small Business Administration (SBA.gov) and state business portals, failing to meet local insurance requirements can lead to license suspension or fines. Always check with your state’s Department of Insurance or local city clerk’s office for compliance.

Financial Protection from Common Risks

Operating a food truck means dealing with open flames, sharp tools, and moving vehicles—all high-risk environments. Food truck insurance helps cover the cost of:

- Accidents on the road (e.g., collisions while driving to an event)

- Fires caused by cooking equipment

- Slip-and-fall injuries from wet floors or uneven pavement

- Food poisoning or contamination claims

- Theft or vandalism of your vehicle or equipment

- Equipment breakdowns that interrupt your business

These risks aren’t just possibilities—they’re common in the mobile food industry.

Event & Venue Requirements

If you plan to attend festivals, concerts, or even local farmer’s markets, many organizers will require a certificate of insurance (COI) that lists them as an additional insured. Without proper coverage, you may not be allowed to participate—no matter how good your food is.

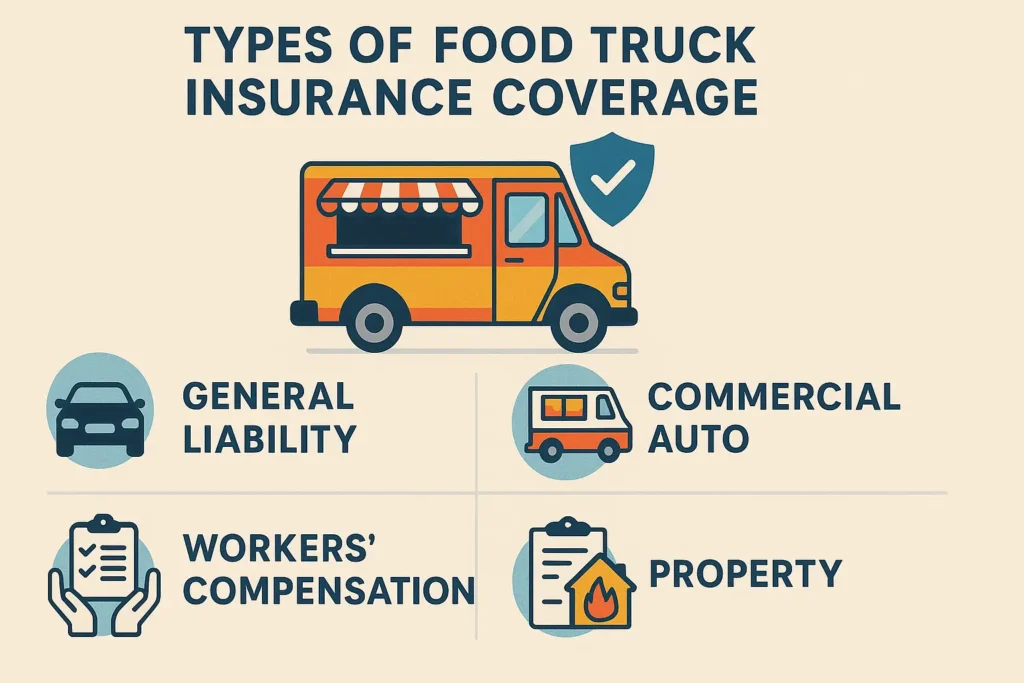

Types of Food Truck Insurance Coverage

Every food truck business is unique, but the risks are consistent—fires, accidents, customer injuries, and equipment breakdowns. That’s why most food truck insurance policies are a combination of multiple coverages tailored to your business needs.

Most essential types of food truck insurance coverage every operator should consider:

1. General Liability Insurance

This is the most important and widely required form of insurance for food trucks. It covers third-party bodily injury, property damage, and legal defense costs.

Example: If a customer slips on a wet spot near your truck and sues you, general liability helps cover medical expenses and legal fees.

Required by most cities and event organizers

Often requested when applying for a health permit or vendor license

2. Commercial Auto Insurance

Since your food truck is also a vehicle, it requires commercial auto insurance—even if you only drive short distances. It covers damage from accidents, collisions, vehicle theft, and property damage caused while driving.

Example: If you rear-end another vehicle on your way to a catering gig, this policy covers repair costs and liability.

Most states require this coverage by law for any commercial vehicle (National Association of Insurance Commissioners)

3. Business Property Insurance

This coverage protects the physical assets inside your truck, such as stoves, fryers, grills, refrigerators, and POS systems. If these are stolen or damaged by fire, flood, or vandalism, property insurance helps replace or repair them.

Example: A generator fire damages your deep fryer and electrical system—property insurance covers the repair costs.

4. Workers’ Compensation Insurance

If you have employees, most states legally require workers’ compensation. It helps cover medical bills, lost wages, and rehabilitation costs if a staff member is injured while working.

Example: A cook burns their hand on a grill—workers’ comp pays for hospital treatment and time off.

Check with your state’s Department of Labor to see if coverage is required.

5. Product Liability Insurance

This coverage helps if someone claims they got sick from your food. It protects you from lawsuits related to foodborne illness or allergic reactions caused by items served from your truck.

Example: A customer sues you claiming food poisoning from undercooked chicken—product liability helps cover legal fees and settlements.

6. Business Interruption Insurance

If your truck is damaged and you can’t operate for a few weeks, this policy can help replace lost income during downtime. It’s especially useful if your vehicle or equipment is out of service due to fire, theft, or major repairs.

Also Read: Ditto Insurance Review: Is Ditto a good company?

How Much Does Food Truck Insurance Cost in 2025?

When budgeting for your food truck business, insurance is a must-have expense—and thankfully, it’s more affordable than many think. In 2025, the average cost of food truck insurance in the U.S. ranges between $2,000 to $4,500 per year, depending on your coverage, state, and business setup.

But remember: the total price you’ll pay depends on a combination of factors unique to your operation.

Average Monthly & Annual Food Truck Insurance Costs

| Coverage Type | Monthly Estimate | Annual Estimate |

|---|---|---|

| General Liability | $25 – $80 | $300 – $960 |

| Commercial Auto Insurance | $70 – $200 | $840 – $2,400 |

| Workers’ Compensation | $50 – $150 | $600 – $1,800 |

| Property & Equipment Insurance | $30 – $100 | $360 – $1,200 |

| Product Liability | Often included | May be bundled |

| Business Interruption | $20 – $60 | $240 – $720 |

| Full Package (Bundled) | $165 – $375 | $2,000 – $4,500 |

Source: Industry averages from providers like Progressive Commercial, Insureon, and Tivly (as of 2025). Always compare quotes for exact pricing.

Key Factors That Affect Food Truck Insurance Rates

- Location (State & City)

Insurance costs vary significantly between states. For instance, rates in California or New York are often higher than those in Florida or Texas due to local laws and population density. - Type of Food Served

Riskier food types (like raw meat or seafood) may raise your liability premiums. - Equipment Value

A truck with $50,000 in kitchen gear will cost more to insure than a basic mobile cart. - Driving History & Claims

Clean driving and insurance claim history can qualify you for discounts. - Number of Employees

More staff = higher workers’ compensation premiums. - Coverage Limits & Deductibles

The more coverage you want—and the lower your deductible—the higher your premium.

How to Lower Your Food Truck Insurance Costs

- Bundle policies with a single provider

- Raise your deductible (if you can afford higher out-of-pocket costs)

- Pay annually instead of monthly to save on processing fees

- Maintain a clean driving record

- Install safety equipment like fire extinguishers and GPS tracking

- Ask about discounts for first-time business owners or veteran-owned businesses

Best Food Truck Insurance Providers in 2025

Choosing the right insurance provider can make or break your food truck business when things go wrong. The best providers in 2025 offer affordable, customizable coverage specifically tailored for mobile food vendors—and many allow you to get a quote online in minutes.

Below is a comparison of the top food truck insurance companies based on cost, features, and ease of use.

Top 5 Food Truck Insurance Providers (2025)

| Provider | Starting Cost | Best For | Key Features |

|---|---|---|---|

| FLIP Insurance | $25/month | Budget-friendly liability coverage | Food truck-specific policies, no deductible, COI in minutes |

| Progressive Commercial | $70/month | Comprehensive auto + liability | Bundle options, strong mobile business reputation, 24/7 claims service |

| Tivly | Varies | Quote comparison tool | Connects you with top-rated providers, personalized agent support |

| Thimble | $15/day or $50/month | Short-term or event-based coverage | Hourly, daily, or monthly options; great for seasonal or part-time vendors |

| CoverWallet | Varies | Customizable, bundled policies | Online quotes, digital COIs, bundled coverage for property, auto, and liability |

Best Providers by Need

- Best for Small Startups: FLIP Insurance – Simple, cheap, and built for food trucks

- Best for Full-Time Operators: Progressive – Reliable and widely accepted across the U.S.

- Best for Event-Based Vendors: Thimble – Offers flexible short-term plans

- Best for Comparing Multiple Quotes: Tivly – Lets you shop and compare from top companies

- Best for Custom Bundles: CoverWallet – Ideal for complex or high-value trucks

What to Look for in a Provider

When comparing food truck insurance companies, consider:

- Does the provider specialize in mobile businesses?

- Can you get a Certificate of Insurance (COI) quickly for event organizers?

- Are there bundling options for auto, liability, and equipment?

- Is customer support available if something goes wrong on the road?

Tip: Always ask for quotes from at least 2–3 providers before committing. You can often save hundreds by bundling policies or switching based on updated coverage needs.

Many providers offer online quotes in less than 10 minutes—no paperwork required.

How to Get a Commercial Food Truck Insurance Policy

Securing the right food truck insurance policy doesn’t have to be complicated. In fact, many providers make the process fast and fully online in 2025. Whether you’re just starting your mobile food business or upgrading your coverage, you’ll want to follow a few key steps to ensure you get the protection you need—at the right price.

Step-by-step breakdown of how to get commercial food truck insurance:

Step 1: Know What Coverage You Need

Before you shop around, get clear on your coverage needs:

- Do you need only liability insurance, or full coverage including auto, equipment, and workers’ comp?

- Will you be working events or fairs that require proof of insurance (COI)?

- Do you employ staff or have valuable cooking gear onboard?

If you’re unsure, request a policy review from a licensed agent or use a provider like Tivly to compare tailored quotes.

Step 2: Gather Your Business Info

To get an accurate quote, you’ll need basic information ready, including:

- Business name, address, and contact info

- Vehicle details (VIN, make, model, usage type)

- List of cooking equipment onboard

- Estimated annual revenue

- Number of employees (if applicable)

- Driving record (for commercial auto coverage)

Pro Tip: If your food truck is leased or financed, your lender may require specific minimum coverages.

Step 3: Compare Quotes Online

Use online platforms like:

- Progressive Commercial

- FLIP Insurance

- Tivly

- CoverWallet

Many allow you to get food truck insurance quotes online instantly, without phone calls or in-person meetings.

Step 4: Review Policy Terms Carefully

Before you purchase:

- Check coverage limits and exclusions

- Look for deductibles and how claims are handled

- Ensure you’re getting the Certificate of Insurance (COI)

- Verify cancellation/refund terms

Don’t hesitate to ask questions—insurance agents are legally required to explain policy details.

Step 5: Purchase & Download Your Policy

Once you’re confident with your coverage and provider, purchase your policy and download your COI immediately—you’ll need this for most city permits and event registrations.

Most providers also allow you to manage your policy, download additional COIs, or make changes online through a digital dashboard.

Step 6: Reassess Coverage Annually

As your business grows, revisit your insurance needs every 12 months:

- Hiring staff? Add workers’ comp.

- Got a new truck? Update your commercial auto policy.

- Serving alcohol or attending more events? You may need expanded liability.

How to Save Money on Food Truck Insurance

Let’s face it—insurance is one of the necessary costs of running a food truck. But that doesn’t mean you have to overpay. With the right strategy, you can significantly reduce your premiums without sacrificing essential coverage. Whether you’re a startup or a seasoned operator, these money-saving tips for food truck insurance can help you stay within budget.

1. Bundle Your Coverage with One Provider

Most food truck owners need multiple policies (general liability, commercial auto, property, etc.). Many insurers offer multi-policy discounts when you buy everything from one company.

Example: Progressive offers discounts when bundling commercial auto and general liability insurance.

2. Increase Your Deductible

Raising your deductible (the amount you pay out-of-pocket before insurance kicks in) can lower your monthly premium.

- Pro tip: Only raise your deductible if you have emergency funds set aside to cover it.

3. Pay Your Premium Annually Instead of Monthly

Many insurance companies offer discounts if you pay your premium for the full year upfront instead of in monthly installments.

- Why? It reduces their processing costs and risk of cancellation.

4. Maintain a Clean Driving Record

Your driving history plays a major role in your commercial auto insurance rate. Avoiding speeding tickets and at-fault accidents helps keep your premiums low.

If you hire drivers, run background checks to avoid risk-based premium hikes.

5. Install Safety Equipment and Security Measures

Installing GPS tracking, dash cams, fire suppression systems, or anti-theft devices can lower your rates.

- Some insurers offer discounts for trucks equipped with fire extinguishers, lockable storage, or security cameras.

6. Avoid Filing Small Claims

While insurance is there for emergencies, filing small claims too often can raise your future premiums.

- If a repair or incident is manageable out-of-pocket, consider not filing a claim.

7. Ask About Special Discounts

Always ask your provider about available discounts. You may qualify for savings if you’re:

- A veteran-owned business

- A new customer

- A long-time customer

- A food truck operating seasonally

- A member of a professional association (like the National Food Truck Association)

FAQs About Commercial Food Truck Insurance

Do you need insurance for a food truck?

Yes. If your food truck operates in the U.S., you’re almost always required by law to have at least commercial auto insurance and general liability insurance. Many cities also require proof of coverage before issuing food vendor permits. Without it, you may face fines or be denied business licenses.

How much does food truck insurance cost per month?

On average, food truck insurance costs between $100 and $300 per month, depending on your location, type of food served, value of the vehicle and equipment, and coverage limits. Bundling policies and maintaining a clean record can help lower this cost.

What type of insurance is best for a food truck business?

The best insurance coverage usually includes a combination of:

1. General Liability Insurance – Covers injury or property damage to others

2. Commercial Auto Insurance – Covers your vehicle and accident-related liability

3. Property Insurance – Covers food truck equipment and inventory

4. Workers’ Compensation Insurance – Required if you have employees

5. Business Interruption Insurance – Helps replace lost income due to unexpected downtime

Is food truck insurance tax deductible?

Yes. According to the IRS, business insurance premiums are a deductible business expense under IRS Publication 535. Keep records of all policy payments and consult with a tax professional for accurate reporting.

Can I get short-term food truck insurance for events or festivals?

Absolutely. Some insurers offer event-based or temporary insurance, perfect for seasonal or part-time vendors. This type of policy can provide liability coverage for just a few days or weeks—ideal if you’re testing the waters or only operate during certain months.

What documents do I need to apply for food truck insurance?

Most insurers will ask for:

1. Vehicle registration and value

2. Type of food sold and cooking equipment used

3. Estimated annual revenue

4. Number of employees

5. Business location and operating zones

6. Claims history (if any)

Being honest and thorough helps you get accurate quotes fast.

Is food truck insurance different from restaurant insurance?

Yes. While both share some similarities, food truck insurance must also cover vehicle-related risks, like accidents or roadside operations. Restaurant insurance usually focuses on property liability inside a fixed location.

What insurance do I need to park at a farmers’ market or fair?

Most event organizers will require:

1. General Liability Insurance (usually $1M minimum coverage)

2. Certificate of Insurance (COI) listing the venue or organizer as “additional insured”

Failure to provide this can result in being denied entry, even if you’re fully licensed.

Conclusion: Protect Your Food Truck Dream the Smart Way

Running a food truck in 2025 is more than just cooking great food—it’s about protecting your mobile business from the unexpected. From liability claims to vehicle damage, food poisoning, or equipment breakdown, one uninsured event could cost you everything.

That’s why food truck insurance is not just a recommendation—it’s a necessity. Whether you’re just starting out or scaling to multiple trucks, having the right coverage helps you stay compliant with state laws, gain entry into premium events, and protect your hard-earned investment.

With providers like FLIP, Progressive Commercial, and Next Insurance, getting a customized policy is easier than ever—often entirely online. And by comparing quotes, bundling coverage, and maintaining a clean claim history, you can even keep your premiums affordable.

If you’ve ever asked, “Do I need insurance for a food truck?” — the answer is yes, and the time to get covered is now.